Swiss Prime Site reports strong results in the first half of 2025 – focus on two pillars is paying off

Ad hoc announcement pursuant to Art. 53 LR

PRESS RELEASE

Zug, 21. August 2025

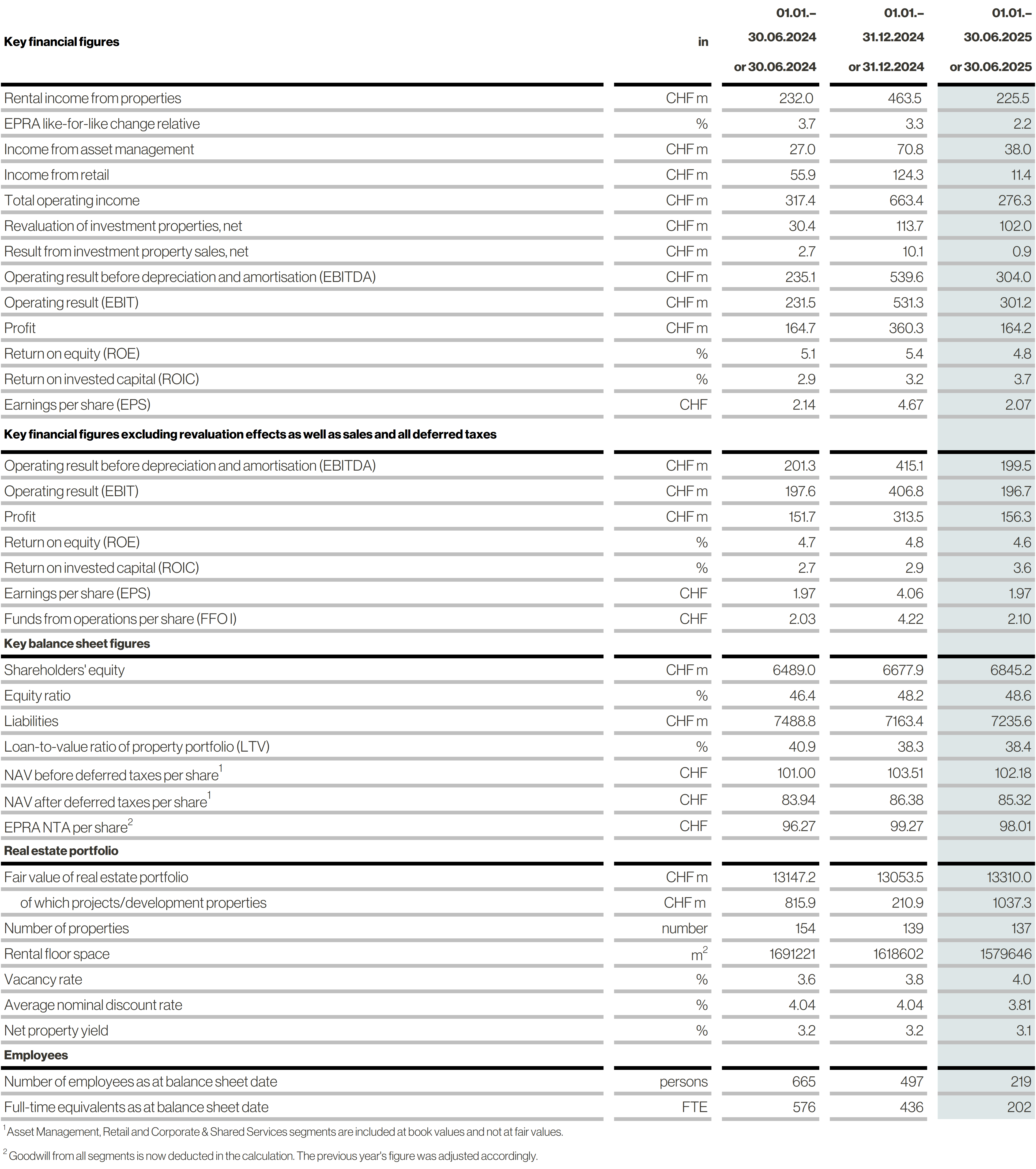

- Increase in funds from operations (FFO I) per share by 3.4% to CHF 2.10

- Growth of total real estate assets to CHF 27.0 billion, including CHF 13.3 billion in Swiss Prime Site’s own portfolio [CHF 13.1 billion as at year-end] and CHF 13.7 billion in Asset Management [CHF 13.3 billion as at year-end]

- Total revenues, excluding Jelmoli, rose by 1.7% to CHF 263.7 million

- Rental income increased by 2.2% on an EPRA like-for-like basis; slight temporary decrease of 2.8% in absolute terms to CHF 225.5 million due to various construction projects and sales

- Asset Management revenues up sharply by 41% to CHF 38.0 million with numerous capital raises and transactions and a full-period consolidation of Fundamenta

- Capital increase of CHF 300 million for profitable growth with first acquisitions made; in parallel, capital raises in Asset Management totalling CHF 540 million

- Conservative financing structure with LTV of 38.4%, at the same level as at year-end

- Optimistic outlook – guidance for 2025 financial year confirmed

In the first half of 2025, Swiss Prime Site achieved its set targets and laid the foundation for further sustainable and profitable growth. René Zahnd, CEO of Swiss Prime Site: «With the closure of the Jelmoli department store at the end of February, we have opened a new chapter. With our business model now exclusively focused on real estate, we are seeking to seize more growth opportunities as they arise, including in our core business of directly held real estate in major cities and urban areas. Thanks to our broad expertise and deep roots in the market, we are able to acquire attractive properties in prime locations that make a positive contribution to FFO (funds from operations) or dividends per share. This is reflected in the first half of the year, with the significant 3.4% increase in FFO to CHF 2.10 – despite the higher number of shares as a result of the capital increase.»

Stable rental income despite numerous construction projects

Income from rental of properties increased by 2.2% on a like-for-like basis (per EPRA) in the first half of 2025. Of this, around 1.4 percentage points are attributable to real rent increases (i.e. exclusive of indexation and reduction of vacancies), which highlights the high rent potential in the portfolio. In absolute terms, rental income temporarily fell slightly by 2.8% to CHF 225.5 million in the first half of the year [prior-year period: 232.0]. This reduction is attributable solely to new construction projects – particularly Jelmoli, Fraumünsterpost and Talacker – and sales in the second half of 2024 that were affecting income in 2025. These effects reduced rental income by around CHF 17 million, of which around CHF 9 million from conversion projects was temporary and CHF 8 million from sales was permanent. Swiss Prime Site almost entirely offset these declines with strong internal growth and the three new developments added to the portfolio. The vacancy rate was 4.0% as at the balance sheet date, 0.2% higher than at year-end [year-end 3.8%] but is expected to fall below 3.8% by the end of this year. The weighted average unexpired lease term (WAULT) remained stable as at June 2025, at a comfortable 4.9 years [prior-year period: 4.8 years].

Property portfolio with significant revaluation due to higher net income

On a fair-value basis, the Swiss Prime Site portfolio was worth CHF 13.3 billion as at mid-2025 [13.1 as at year-end]. At half-year, revaluations in the portfolio were at plus CHF 102.0 million or 0.8% [+30.4 in H1 2024]. The discount rate applied by independent real estate appraiser Wüest Partner fell slightly. Hence more than 60% of the positive valuation results were attributable to higher new lettings and other rental effects. Furthermore, Swiss Prime Site will use the funds from the capital increase to further enhance the quality of its portfolio.

Following the extensive divestments in the previous year, Swiss Prime Site continued – on a scaled-back level – its strategy of financing development projects by selling non-core properties (capital recycling or upcycling) as it sold six properties for a total of CHF 70 million. This yielded a profit of 4.1% above the last estimated appraisal value. Three of the six property sales have their closing date after the balance sheet date.

Asset Management: Jump in profits from capital raises and synergies

Asset Management grew strongly again in the first half of the year. A total of CHF 540 million in new issues was subscribed for the various vehicles. Some of the new funds were already invested in the first half of the year. Assets under management (AuM) thus increased to a total of CHF 13.7 billion [CHF 13.3 billion as at year-end]. The acquisition of the specialist Asset Manager Fundamenta also had a positive impact. Overall, the result was a jump in sales by around 41% to CHF 38 million. Despite the numerous transactions, the proportion of recurring income remained high at 72% [80% prior-year period]. Thanks to economies of scale with the full integration of Fundamenta yielding realised synergies of around CHF 4 million, EBITDA increased in the first half of 2025 by 64% to CHF 23.9 million [CHF 14.6 million], which is reflected in a significant increase in the EBITDA margin to 63% [54%].

Operating profit stable, FFO I per share continues to rise

Consolidated operating result (EBITDA) before revaluations and sales remained almost constant at CHF 199.5 million [CHF 201.3 million in the previous year] despite the loss of rental income following the commencement of redevelopment works at the Jelmoli building and other newly started renovation projects. Direct real estate expenses fell significantly, down almost 8%, thanks to the optimised portfolio and stringent cost management.

Total interest expenses fell for the first time since the cycle turn in interest rates in 2022. For the first half of 2025, they amounted to CHF 27.5 million and were 17% below the previous year. At 0.98% [previous year 1.16%], the average interest rate has returned below the one-percent threshold since some time ago. In addition to interest costs, financial expenses include non-cash fair value adjustments to the last outstanding convertible bond in the amount of CHF 65 million, a direct consequence of the significantly higher share price at the half-year close. Overall, profit before revaluations and sales totalled CHF 156.3 million [CHF 151.7 million].

The cash result per share (FFO I, funds from operations) thus rose by 3.4% to CHF 2.10 [CHF 2.03], due to a stable operational profit contribution combined with lower financing costs and taxes. The increase in FFO per share was achieved also with the higher number of shares from the capital increase in February 2025.

Capital increase and stable financing structure

Despite a subscription price with a premium of almost 19% over net asset value, this capital increase of CHF 300 million was oversubscribed several times. The proceeds are to be invested in new «prime» properties by the end of the first half of 2026. A first acquisition at the prestigious Place des Alpes in the heart of Geneva has already been completed, as has an acquisition in Lausanne-West after the half-year close. The capital increase is intended to be used for profitable growth and thus to be value accretive for all shareholders. At 38.4%, the loan-to-value (LTV) ratio was around year-end level.

Interest-bearing financial liabilities excluding leases totalled CHF 5.4 billion as at the balance sheet date [prior year: CHF 5.3 billion]. This financing continues to be drawn from broadly diversified sources on the banking and capital markets. The proportion of unsecured loans rose slightly to 88.1% [year-end: 87.8%], as expiring mortgages were repaid with liquidity and not refinanced. Unutilized, contractually committed credit lines totalled CHF 913 million at mid-year [CHF 1 054 as at year-end], which, together with the unencumbered asset base, guarantees a very high degree of operational and financial flexibility.

Confirmation of outlook

For the full year 2025, management continues to expect the vacancy rate to fall to below 3.8%. The strong momentum in Asset Management should continue in the second half of the year. Given the attractive real estate market, the target of exceeding the CHF 14 billion threshold for assets under management by the end of the year seems more than realistic. At the consolidated level, rental income is forecast to be nearly stable, i.e. it should be possible to compensate for a large proportion of the temporary reduction of rent (from Jelmoli, continued renovation and sales). Also with the additional shares from the capital increase, FFO I per share should be at the upper end of the forecast range of between CHF 4.10 and CHF 4.15.

SELECTED KEY FIGURES

If you have any questions, please contact:

Investor Relations, Florian Hauber

Tel. +41 58 317 17 64, florian.hauber@sps.swiss

Media Relations, Mara Ricci

Tel. +41 58 317 17 42, mara.ricci@sps.swiss

Web links: Press release | Presentation