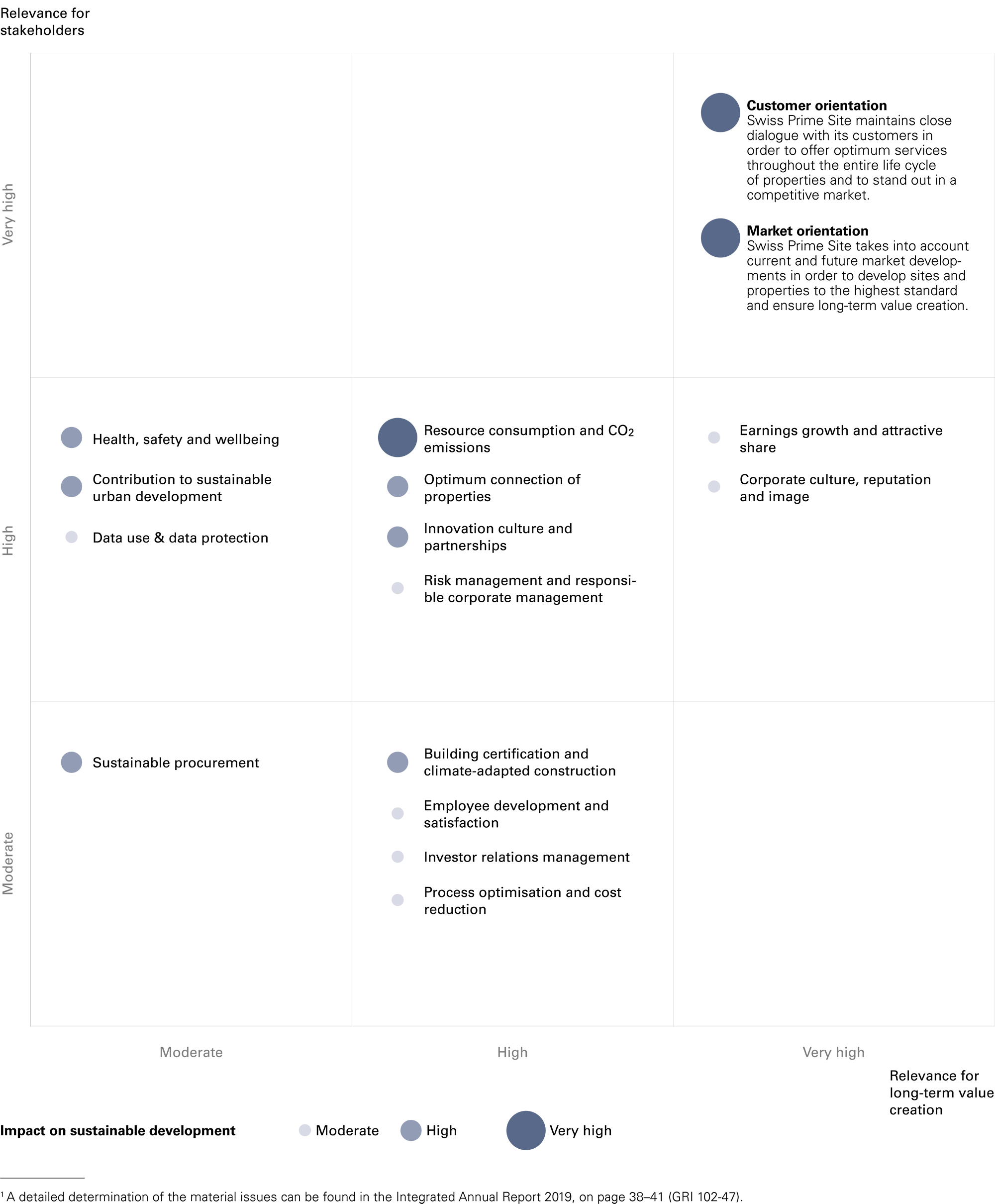

Material issues

In 2019, as part of a comprehensive materiality analysis, Swiss Prime Site determined for the second time since 2017 which issues are particularly important for the further development of integrated management. This enabled the Company to create the basis for the integration of important financial and non-financial issues into the management of the group and defined the strategic focus of integrated reporting (GRI 102-49).

Process for determining the material issues

In the materiality analysis, the aim was to assess how important the particular issue is to the different stakeholders, and to the business success of Swiss Prime Site, and also how important the issue is with regard to the Company’s impact on sustainable development. Assessing business relevance as the third dimension ensures that the material issues are closely related to the core business and can be integrated into strategic management.

Swiss Prime Site arranged the issues in order of materiality according to the six capitals of the International Integrated Reporting Council (IIRC). Adopting the capital-based approach reflects the Company’s wide-ranging aspiration to create sustainable value for the various stakeholder groups from a wide range of resources.

Integration of internal and external stakeholders

In particular, Swiss Prime Site used the materiality analysis to enter into an ongoing dialogue with different internal and external stakeholders. In addition to management representatives, business partners and clients were also consulted about their priorities. Swiss Prime Site also took into account the findings of the 2019 Stakeholder Panel. The next materiality review is scheduled for 2021 (GRI 102-46).

Inclusion of material issues in goal-setting

The materiality analysis serves as a starting point for Swiss Prime Site to make further improvements to the integrated manage- ment of financial and non-financial aspects. In the reporting year, the Company – drawing on the material issues amongst others – defined overall corporate goals, from which they derived measures for the group companies (see Strategy/Sustainability goals). The materiality analysis also defines the focus of this integrated reporting.